Features

How Europe can build on strengths in SEPs to reclaim leadership in cellular with 5G and 6G

28 April 2022

A paper for 4iP Council by Keith Mallinson, WiseHarbor

Europe was once preeminent in cellular communications with 2G GSM—including standard-essential technology innovation, product developments and sales, network deployments, and operator services adoption by consumers. Since its heyday in the in the late 1990s, Europe has declined through a succession of falls from various leading positions in cellular.

The European Commission’s initiatives to regulate standard essential patents (SEPs)—most significantly in cellular technologies and ostensibly for the benefit of SMEs and other technology implementers—are oblivious to this bigger picture. It is vital for all Europeans that the region’s remaining major players in the cellular ecosystem can flourish profitably and are able to continue investing in R&D for innovation, new products, network deployments and services growth. That means ensuring standard-essential technology developers including the European Union’s Ericsson and Nokia can make fair and adequate returns on their SEP investments. The SEP licensing system needs to be reinforced, not weakened with prospective interventions that are inconsistent, contradictory or that have weak factual justification and would jeopardise Europe’s competitiveness.

Re-establishing European strength in cellular also requires reregulation of operator and other services markets so that European mobile network operators can become profitable leaders in the mobile ecosystem once again. Hopefully the EU’s new Digital Markets Act (DMA) that seeks to reign-in the dominant and abusive behaviour of Big Tech companies such as Apple, Alphabet and Meta will help European mobile operators and others improve their competitive positions and abilities to become leaders rather than remain followers with new technologies and services. Anticipated measures against these Big Tech “gatekeepers” include restrictions on bundling and self-preferencing between complementary services (e.g. search versus shopping), and mandating interoperability among different messaging platforms.

Call for action and evidence

In November 2020, the “[European] Commission published a new Action Plan on Intellectual Property to help companies, especially small and medium-sized companies (SMEs), to make the most of their inventions and creations and ensure they can benefit our economy and society”. Including various types of intellectual property, the Action Plan sets the Commission’s main steps amongst others to “improve the protection of IP”, “boost the uptake of IP by SMEs” and “facilitate the sharing of IP to increase the technological uptake in the industry”.

Despite guidance provided in its 2017 Communication ‘Setting out the EU approach to SEPs' the Commission “observe[s] continued friction in the uptake of SEP-protected standards. In addition, the landscape gets more complex as we move to 5G and beyond, and the number of SEPs, as well as the number of SEP holders and implementers, are increasing”.

In February 2022, the Commission initiated a call for evidence for an Impact Assessment regarding a new framework for standard-essential patents. In this it reiterated and expanded that:

“SEP licensing is not seamless and called for a balanced approach based on an increased transparency. The Commission gave guidance to the standards industry and announced a set of actions to analyse the situation. The Commission has thus: (i) conducted a number of studies; (ii) set up an expert group on the licensing and valuation of SEPs; and (iii) monitored the market situation. Despite some improvements since 2017, there continue to be significant disagreements among stakeholders with regard to SEP licensing” (Citations omitted).

The Commission also reminded us that its IP Action Plan “announced that it would further promote transparency and predictability in SEP licensing, including by possibly reforming the SEP licensing system” (emphasis added).

This is all prompting fervent response in the runup to the call for evidence submission deadline on 9th May 2022. For example, one commentator opines that the EU “rolls the dice with its push on standards and SEPs”, and that “[d]espite having positive elements, these initiatives present significant challenges: they are occasionally inconsistent or contradictory, while some proposals have a weak factual basis and could entail risks for EU leadership in standardisation”.

Broader context and strategies

In a March 2022 keynote speech at the Mobile World Congress in Barcelona, Vodafone’s CEO Nick Read described 5G as the catalyst for innovation—transforming every industrial sector and will underpin the next phase of the digital society. He said that every country and region will try to maximize their chance to capture this opportunity for jobs and growth.

But Europe has fallen far behind in 5G deployments and in other technology markets. Read noted that 5G coverage is above 90% in South Korea, at around 60% in China and 45% in the US, and at less than 10% in Europe. It is also South Korean, Chinese and American original equipment manufacturers (OEMs) that account for the overwhelming majority of smartphone sales globally, including those incorporating 5G. While eight of the world’s 10 most valuable companies including Apple, Microsoft, Alphabet and Meta are tech firms, Europe’s most valuable company — Dutch chip foundry equipment maker ASML — ranks only 32nd globally.

China has propelled itself to the forefront of cellular standards development, patenting, product implementation and in network deployments. Chinese industrial policy is achieving that through initiatives including Made in China 2025, China Vision 2035 and China Standards 2035. Chinese operators have received their 5G spectrum without paying substantial fees for it, as are commonly generated through auctions in many nations and that have hobbled the ability of European operators to invest in improving their networks since the millennium.

Even though the US is also still divided in how it deals with SEPs, it has at least instigated more coherent and successful industrial policies in other aspects of 5G development and its Big Tech platforms have extracted much of the value in the cellular ecosystem since the smartphone revolution began with introduction of the iPhone in 2007.

Europe also needs a more joined-up strategy to re-establish a position of strength, let alone leadership in cellular technologies including the Internet of things (IoT). SEP development and licensing has worked well by providing a stable and vital source of income to standard-essential technology developers, and a flow of innovative new capabilities to product implementers, network operators and consumers worldwide. Rather than meddle with that where objectives and benefits are doubtful, Europe needs to fix things elsewhere.

From trail blazer to trailer

The development of cellular technologies and their markets exemplify humanity’s greatest technical, economic and social success of the last century. Global competition and coordination have brought relentless innovation and enormous utility at low cost to 5 billion people worldwide. Most of these have smartphones that provide them with their primary—if not only—access to the Internet for information and entertainment, as well as essential voice and messaging connectivity. 5G promises to expand personal communications to include orders of magnitude more connections and superlative performance in IoT.

Cellular technologies and markets have developed in a series of generations from 1G analogue to 5G today, and with 6G upcoming commercially around 2030. The principal contributors and commercial beneficiaries have shifted at each stage with Europe forging a preeminent position in 2G, followed by its continuous decline ever since.

Fragmented yet lucrative markets for several in 1G

Analogue (1G) mobile network operators in the 1980s and early 1990s were mostly national monopolies with “licenses to print money”, such was the price-insensitive demand from business users and social elites in nations with poor fixed network infrastructures, such as in Eastern Europe.

Network equipment and device suppliers thrived, but within the confines of national and regional markets due to a patchwork of different technology standards. For example, France and Germany had their own national standards and Nordic standard equipment was incompatible with standards used in the US, UK and Japan.

Globalization commences with competing operators and oligopoly in 2G technology supply

Second rounds of licensing introduced 2G with competing operators. With only duopolies at first, these were also able to grow very profitably under the strength of their own cashflows.

The most successful technology suppliers were the handful of European companies that developed the GSM standard which was mandated across Europe in conjunction with the EU’s programme for “completion of the single market” in 1992. Whereas GSM started as a European project named after a committee called Groupe Spécial Mobile, the acronym’s definition was changed to Global System for Mobile as the standard was positioned to lead and then dominate globally. Cross-licensing or non-assertion among developers of GSM’s standard-essential technologies entrenched the market positions of European companies including Nokia, Ericsson and Siemens. In contrast, outsiders such as Japan’s NEC were marginalized despite it being a leader in the UK’s 1G mobile phone market. Nokia captured most of the mobile phone market’s total global profits with GSM sales from the mid-1990s until the mid-2000s.

High spectrum charges, lacklustre demand for 3G and demise of the GSM suppliers club

Flush from success with 2G GSM—and with excitement about the possibility of surfing the net on a mobile phone—3G UMTS was overhyped prior to European service launches from around 2003. The technologies and ecosystems were not ready to deliver what was required to fulfil that promise. European operators paid a high price with introduction of yet more competitors and high spectrum fees totalling $150 billion from around the millennium. This shock was also at a particularly hard time with the dotcom market crash.

What consumers actually wanted and valued in a mobile phone—as European 3G networks were being rolled out—was epitomized by the 2004 introduction of the highly successful 2G Motorola RAZR. The phone’s main attribute was that it was thin. This precluded 3G at that time, but the device did have a camera, colour screen and polyphonic ring tones. This was a one-off big hit for the company that decade.

European technology developers including Ericsson, Nokia and the European firms they subsequently acquired remained major contributors to technology developments, though accepting Qualcomm’s leading contributions to the 3G UMTS standard with various patented CDMA technologies.

While Nokia continued to capture most of the mobile phone market’s total profits with 2G and 3G sales until the late 2000s, the introduction of the 2G iPhone in 2007, a 3G iPhone and 3G Android phones in 2008 was the beginning of the end for Europe’s broad-based leadership in cellular.

Europe fell further behind with migration to 4G LTE and 5G

Even though European companies have continued to be leading developers of cellular standard-essential technologies and suppliers of network equipment including those technologies, the value derived from all that has increasingly been captured by other suppliers.

Europe’s collapse in the cellular devices business with the notable market exit of handset vendors including Bosch (2000), Philips (2001), Alcatel (2005), Siemens (2008), Ericsson (2011) and Nokia (2014) was nothing to do with SEP licensing mechanisms and costs. To the contrary, these European OEMs were all significant cellular SEP owners and licensors. As these companies were failing in the handset business there was extensive market entry by many other handset vendors that had little or nothing in the way of cellular SEP ownership. Market disruption has continued with significant market entry by Chinese smartphone OEMs Xiaomi (2013), Oppo (2014) and Vivo (2014) that have all risen into the top 5 globally.

Silicon Valley’s Big Tech companies including Apple, Alphabet and Meta have also gained enormously from the smartphone revolution including the transition to 4G and 5G over the last decade. Apple has taken the majority of the mobile phone market’s total profits every year since 2011. As with the fixed Internet, it is the America’s Big Tech platforms including Apple with its iOS operating system and App Store, Alphabet with Android and Google Play, Meta with Facebook and various other over-the-top (OTT) apps (e.g. Netflix and Uber) that have monetized mobile most effectively. Their revenues and profits have soared, largely due to smartphone communications.

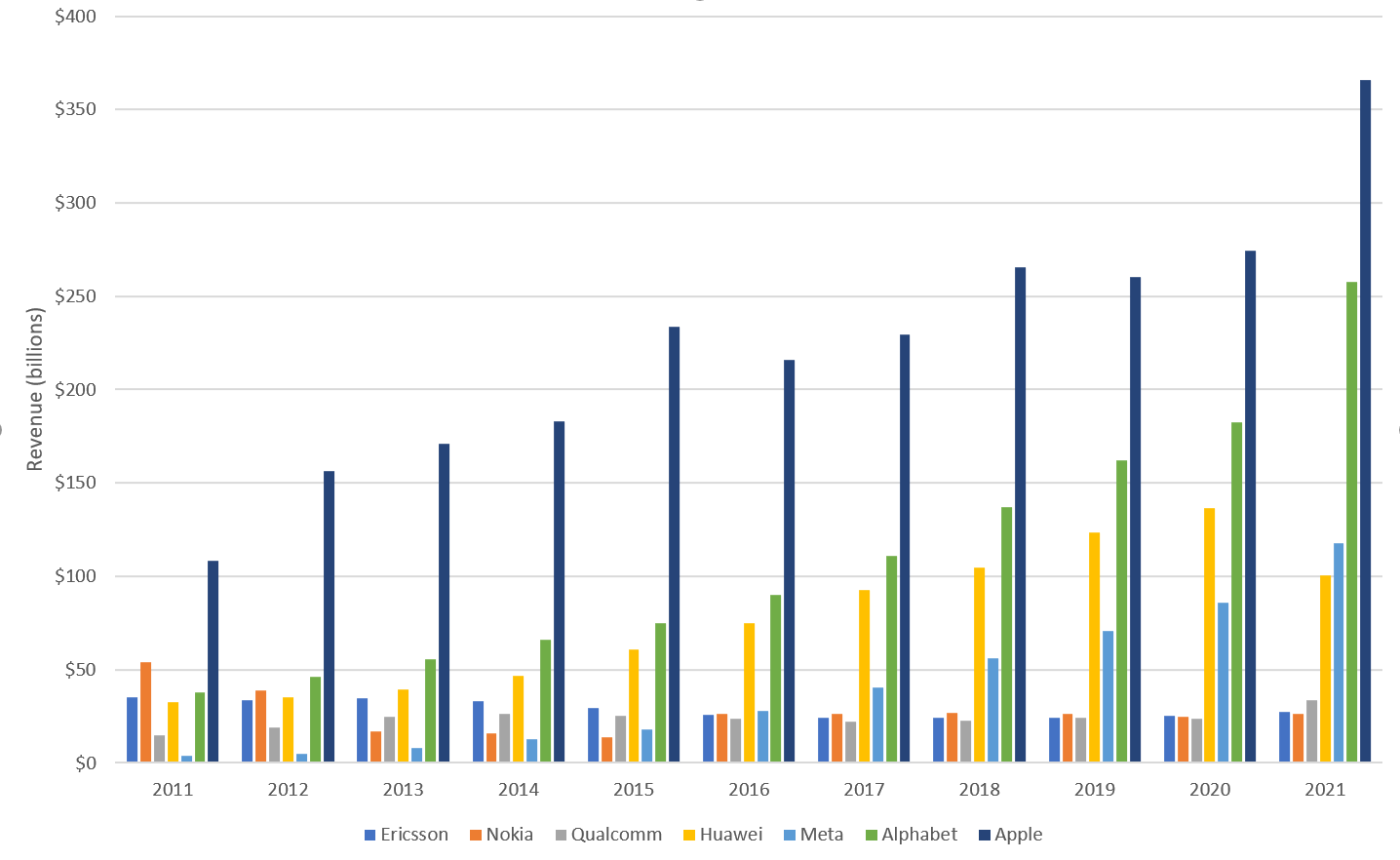

Exhibit 1: Revenue growth captured in cellular by newcomers from outside Europe

Source: Companies’ yearend reports and average annual exchange rate figures

The competitive threat to European companies is that these Big Tech platforms continue to grow and take an increasing share of ecosystem profits with their expanding range of services including Alphabet’s Google Cloud, and cloud services from the others including Amazon’s AWS and Microsoft’s Azure. European cellular OEMs and operators are becoming encircled by and heavily dependent upon these larger and more profitable players. These cloud services are increasingly being used to host mobile operators’ core network and radio access network computing.

The major competitive blow to European mobile technology innovators and product suppliers, including its remaining world leaders Ericsson and Nokia, has come with the advance of Chinese firms. While all firms are dependent on multilaterally developed global standards, China is increasingly self-contained in supply of network equipment and with its own Big Tech platforms including JD.com, Alibaba and Tencent, as well as in devices.

Technologies and products provided by Nokia and Ericsson, as well as Qualcomm, InterDigital and others are essential enablers for the entire cellular ecosystem, even though these firms generate modest revenues and profits in comparison to Big Tech companies downstream. The SEP licensing revenues generated by the former are vital for them to flourish, or even to survive.

Europe’s mobile operators have also fared worse than leaders in US, China, South Korea and Japan

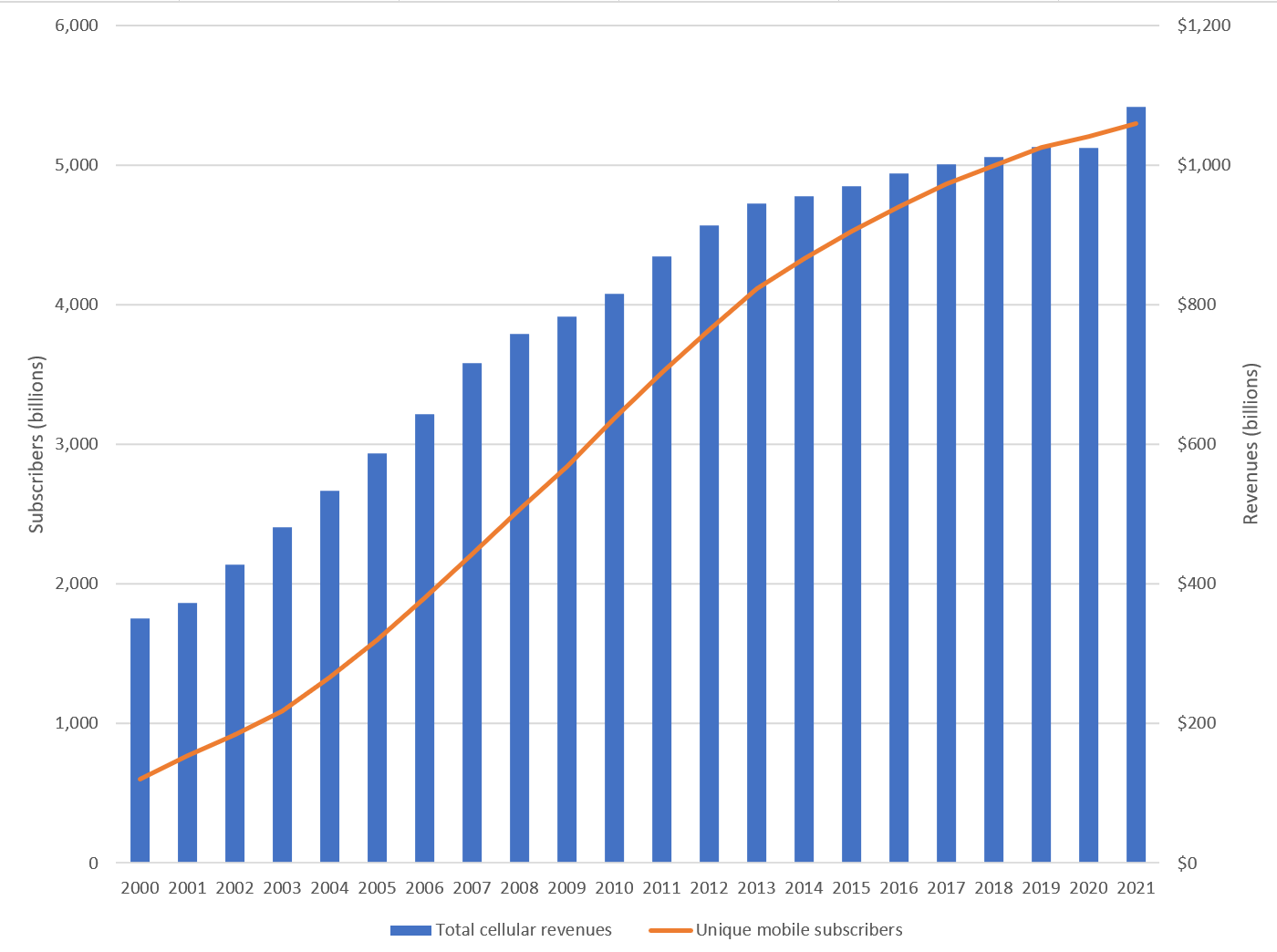

Despite inflation of a few percent, global mobile operator services revenues have only grown a couple of percent per year over the decade to 2020 while numbers of subscribers have increased at more than twice that rate. With the worst of the pandemic over and with a boost from 5G’s early adopters there was a stronger revenue uptick in 2021.

Exhibit 2: While the number of cellular subscribers globally has continued to grow, total operator revenues flattened in the decade to 2020

Source: GSMA Intelligence

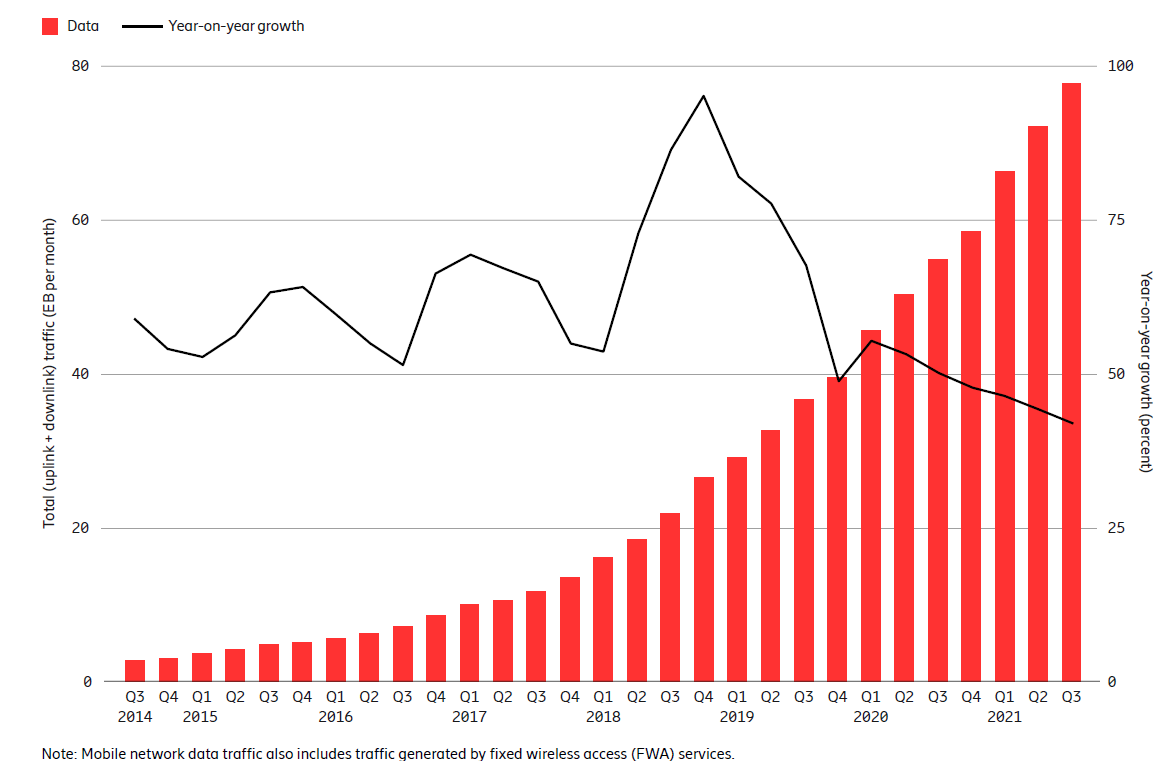

Meanwhile, network data traffic has doubled every couple of years.

Exhibit 3: Total data traffic has doubled very couple of years

Source: Ericsson Mobility Report

The financial performance of European mobile network operators has been limited by huge capital investment demands—with several operators competing in every nation—and with obligations to provide limitless free connectivity to the Big Tech platforms under net neutrality requirements in a series of network upgrades and expansions.

The major differences in national 5G deployments reflect market conditions. Concentrated operator markets in US, China and South Korea—each with only three major national networks competing as 5G was commencing in 2020—have generally enjoyed rather healthier financial conditions and better ability to invest than in Europe where more operators compete in less lucrative markets.

SEP licensing in an expanding ecosystem

Standard-essential technologies upon which standards such as 5G are built are the lifeblood of market development for the entire cellular ecosystem including products, operator services and OTT applications. As the cellular industry has become less vertically integrated, increasing numbers and types of company downstream depend on the relatively small number of firms that develop most standard-essential technologies.

SEP licensing is vital to those that develop standard-essential technologies and are not implementers in the devices markets. Export revenues from licensing by Ericsson and Nokia—of around $2.7 billion in 2021—were overwhelmingly for implementation of cellular SEPs by Apple and Asian device manufacturers. SEP royalties fund continued R&D (they spent nearly $10 billion on that in 2021) to maintain know-how and leadership in cellular communications technologies and standards development.

However, there is a longstanding schism on SEP licensing issues. Major handset OEMs and various operators have repeatedly sought to minimize SEP licensing fees. Even though most licenses are agreed without dispute, litigation about royalty rates between these OEMs and licensors has been significant. For more than 15 years, Next Generation Mobile Network association membership has conspired with initiatives to cram down royalty rates paid. Prior to the introduction of LTE around 2010 it contrived a process that erroneously projected aggregate royalty rates generally in excess of 30%. Allowing members to report their maximum rates anonymously and without the need for explanation led to significant inflation in reported rates. This purported royalty stack was referenced in attempts to reduce the royalty demands of individual licensors.

In contrast, I have showed since 2015 that actual rates paid including LTE and other technologies were no more than around 5% of handset prices and that aggregate rates paid to major licensors have declined in recent years. Subsequent assessments have this figure at around 3% with total royalties of around $15 billion per year. Licensing costs pale in comparison to total revenues and profits derived as the cellular ecosystem expands to be worth many trillions of dollars in products, services and applications including IoT.

Phony grass-roots activism

Various allegations of threats and harm to implementers, operators and consumers through SEP licensing are bogus. SMEs are rarely the target for SEP licensors for various reasons. For example, European SMEs in particular are more likely to be software developers that do not need to license SEPs than device or module manufacturers that do need to be licensed. All the top 5 IoT module manufacturers—accounting for more than 50% of shipments—are Chinese. These are the priority for any SEP licensing in IoT. There is no empirical evidence SMEs are being significantly pursued for licensing or being shut down for use of SEPs. It is the large implementers that resist paying even modest fees that are sued. Some of their countermeasures include outright deception.

For example, for what is now increasingly referred to as “astroturfing”, the Association for Competitive Technology—ACT | The App Association—which purportedly represents the interests of SME technology companies—was unmasked as a front promoting interests of Big Tech firms including monopoly gatekeeper Apple. While Apple litigates to maintain its 30% markup on third-party sales through its App Store, it seeks to crush the few percent paid to license SEPs despite making profit margins an order of magnitude higher on its iPhones.

Making not undermining a European renaissance

While no system is perfect, injecting greater uncertainties is more likely to hinder than help Europe re-establish global leadership in cellular. Its globally competitive position with strength in SEP development and network equipment sales by Ericsson and Nokia should be preserved and reinforced. The opportunity is for growth from new technologies is in 5G Advanced, 6G, IoT, the cloud, the metaverse, edge computing and artificial intelligence. Europe needs to build on—not undermine—its existing strengths with joined-up strategies to capitalise on all the new opportunities.

The DMA holds some promise to constrain the market power of Big Tech firms that are taking the lion’s share of ecosystem profits, but these incumbents will be difficult to displace. European companies need help on many different fronts to compete more effectively against these, capitalize on new technologies and seize market opportunities.

Policy makers should be wary of messing up the established balance in SEP licensing, and should address more significant and fundamental shortcomings that have impeded growth in the European cellular ecosystem and eroded the region’s competitive position. The European Commission’s extensive proposals to regulate SEP licensing are myopic and without consensus in strategic purpose or priority versus more fundamental and greater shortcomings in European 5G.

As reflected in the dissenting opinion of Monica Magnusson, Vice-president, IPR Policy Ericsson, one of the, Group of Experts on Licensing and Valuation of Standard Essential Patents ‘SEPs Expert Group’ “the group did not identify and agree on a clear problem statement to direct its work. As a result, different individual experts set out to submit proposals to the problems they perceived warranted solving, rather than focus on topics where consensus could potentially be reached in the group—and, by proxy, where a broader base of support could be expected in the wider licensing ecosystem.”

This is a particularly bad time for the European Commission to weaken SEP licensing. While European SEP owners continue to seek FRAND licensing with recalcitrants including several non-European smartphone OEMs, the EU has launched an WTO dispute against China over telecom patents. Nokia is currently in SEP and FRAND licensing litigation versus Oppo and Vivo and Ericsson is similarly in dispute with Apple.

These two EU companies that command a substantial proportion of total SEP licensing fees have generated around $14 billion from licensing over the last five years. This was vital for their wellbeing and survival. It would be a travesty to jeopardize that with wholesale “reform”, where hoped-for benefits are unquantified, unclear and are likely to be worth far less than the economic harm they may cause.

The EU is in grave danger of “throwing out the baby with the bathwater” in its prospective attempts to reform SEP licensing with interventions to the purported benefit of European SMEs in IoT. Proposals such as institutionalising essentiality checking would be voluminous and very costly. SEP licensing beyond the mobile phones, tablets and a small proportion of laptop or notebook PC shipments is very limited. With less than a few hundred million dollars generated annually so far and with a billion dollars per year worldwide unlikely before 2026—even with high compound annual growth rates of 25%—SEP licensing in European IoT implementation will remain tiny in comparison to the licensing of Apple and Asian device manufacturers. The export income the latter generates is vital for Europe’s competitiveness.

Europe needs to maintain a competitive environment that enables European leaders like Nokia and Ericsson, as well as others to flourish. SEP licensing with fair and adequate payments is agreed by many licensees and is vital for licensors. The problem is with other implementers who steal from patent owners and obtain unfair competitive advantage against licensed implementers by holding out to avoid, delay or reduce payment.

Private solutions to increase and improve SEP licensing are prominent and are making headway. Transparency, predictability, a level playing field (with the same prices for all OEMs), low costs and enormous value is provided with most cellular SEP owners licencing cars through the Avanci platform. For 4G at $15 per car, licensing costs only as much as a car wash. Europe’s BMW, Volkswagen Group and even now Daimler now are leading the world’s OEMs in signing up. Majors elsewhere including market leader Toyota, Hyundai-Kia, General Motors and Ford remain unlicensed. Avanci is a better solution than intervention and reform on a weak factual basis. Monica Magnusson was also critical that “at no point during its two-year mandate did the [Expert Group] analyse, interview or otherwise consider the only (at the date of writing) fully operational patent pool in the IoT space (i.e. Avanci)” (citation omitted).